Environmental Risk Screening for Commercial Real Estate Lenders

Commercial real estate loans can carry hidden environmental risk — especially when the property has a history of fuel sales, dry cleaning, auto repair, industrial use, storage tanks, spills, or cleanup activity. Brownfield.ai helps lenders screen any address for environmental risk in minutes, before small issues become late-stage surprises.

- Sign up, enter address, get results

- First report on us

- No credit card required

How it works

A faster way to spot environmental risk before you commit to a property.

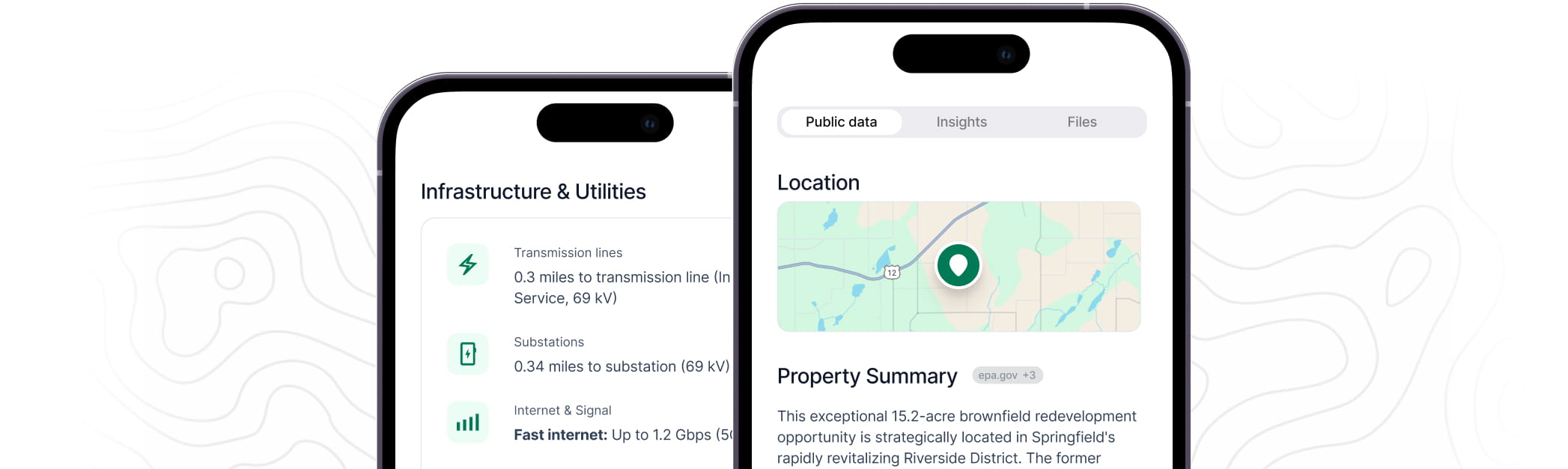

1. Search any address

Create a free account and enter a property address. No forms. No sales call. No waiting.

2. Brownfield.ai checks the records

We scan the environmental databases that matter — EPA, state environmental records, LUST, UST, PFAS, flood zones, cleanup records, hazardous release data, and more.

3. Know the risk before you spend

Get a clear report showing environmental red flags, regulatory issues, contamination indicators, and surrounding property concerns — so your team can ask better borrower questions and decide what needs deeper review.

The Risk Isn't Just the Property. It's Finding Out Too Late.

Most environmental issues do not appear at the perfect moment. They show up after the loan is moving, after the borrower is invested, after underwriting has started, or after the Phase I raises questions no one expected.

A former gas station. A dry cleaner in a retail strip. An auto repair shop with old tanks. A warehouse near known contamination. A commercial property with limited site history.

Any of these can create questions for lenders, especially when the records are unclear.

Brownfield.ai helps lending teams identify environmental risk signals earlier — before the issue slows down underwriting, creates borrower confusion, or forces a last-minute scramble for answers.

What Brownfield.ai checks

For any address, Brownfield.ai scans key environmental and property risk signals, including:

- Leaking underground storage tank records

- Underground and aboveground storage tank indicators

- Historical gas station, auto repair, dry cleaner, and industrial-use indicators

- EPA and state environmental regulatory records

- Known contamination and cleanup activity

- Hazardous release and spill records

- Petroleum, solvent, and vapor intrusion risk indicators

- PFAS and hazardous material indicators

- FEMA flood zone data

- Nearby environmental concerns that may affect the property

- Open regulatory issues or records that may require follow-up

It does not replace a Phase I ESA, environmental questionnaire, lender policy, or consultant review — it helps your team identify potential issues earlier.

Screen a property before environmental risk slows the loan

Enter an address and get an instant environmental risk report.

What Environmental Risk Signals Should Lenders Watch For?

The issue is not always confirmed contamination. The issue is uncertainty. If the borrower, lender, attorney, or consultant cannot quickly understand the site history, regulatory records, cleanup status, or surrounding environmental conditions, the loan may need more review before moving forward.

Watch for:

- Former gas station or fuel sales use

- Former dry cleaner or laundry use

- Former auto repair, body shop, garage, or fleet maintenance use

- Industrial, manufacturing, warehouse, or machine shop history

- Underground or aboveground storage tanks

- Leaking tank records or petroleum releases

- Known cleanup or remediation activity

- Solvent, degreaser, or hazardous material use

- Floor drains, sumps, or oil-water separators

- Nearby properties with known releases or industrial history

- Flooding or stormwater conditions that may affect collateral risk

- Records that could trigger additional lender, insurer, attorney, or consultant review

Know What You’re Lending Against Before the Deal Gets Complicated

A Phase I ESA or formal environmental review may still be required, depending on the loan type, property use, risk profile, and lender policy. But lenders do not have to wait until late in the process to understand obvious environmental risk signals.

Brownfield.ai gives lending teams an earlier read. It helps you identify potential concerns, prepare borrower questions, compare collateral risk, and decide whether deeper environmental due diligence may be needed.

Who it's for

Built for Commercial Real Estate Lenders, Credit Teams, and Loan Officers

Brownfield.ai helps lending teams quickly screen commercial properties before environmental issues slow down underwriting.

Use it if you are:

- Reviewing a commercial real estate loan

- Evaluating collateral with possible environmental risk

- Preparing borrower questions before credit review

- Screening a former gas station, dry cleaner, auto repair shop, or industrial site

- Reviewing SBA, conventional, bridge, construction, or redevelopment financing

- Comparing risk across multiple properties or borrowers

- Trying to identify whether a property needs deeper environmental due diligence

Built for Real-World Lending Workflows

Environmental risk often enters the lending process late. A borrower may not know the full site history. A broker package may omit prior uses. A property may look ordinary from the street but have tank records, cleanup history, nearby releases, or regulatory issues that affect the collateral review.

Brownfield.ai helps lenders surface those questions earlier. You can use the report to prepare borrower follow-ups, flag issues for internal review, support consultant conversations, and reduce surprises before the deal gets too far along.

Frequently Asked Questions

Does Brownfield.ai replace a Phase I ESA?

No. Brownfield.ai does not replace a Phase I Environmental Site Assessment, lender environmental policy, environmental questionnaire, or consultant review. It is an early screening tool that helps lenders identify potential risk signals before deciding what deeper review may be needed.

Why should lenders screen environmental risk early?

Screening early helps lenders identify red flags before underwriting, credit review, borrower conversations, or closing timelines are affected. It can also help teams ask better questions and avoid late-stage surprises.

What types of commercial properties should lenders screen?

Lenders should consider screening properties with current or historical uses that may create environmental risk, including former gas stations, dry cleaners, auto repair shops, body shops, fleet maintenance sites, industrial properties, warehouses, vacant commercial sites, and properties near known contamination.

What does Brownfield.ai check?

Brownfield.ai scans environmental and property risk signals from sources like EPA records, state environmental records, LUST records, UST records, cleanup records, hazardous release data, PFAS data, FEMA flood zones, and other relevant public databases.

Can Brownfield.ai help with SBA loan review?

Yes. Brownfield.ai can help identify environmental risk signals before or during SBA-related property review. Lenders should still follow SBA requirements, internal policy, and consultant recommendations.

Will Brownfield.ai tell me whether to approve or decline a loan?

No. Brownfield.ai does not make credit decisions. It helps identify known environmental risk signals so lenders can make more informed decisions, ask better questions, and decide whether further review is needed.

Can I use Brownfield.ai before ordering a Phase I ESA?

Yes. Brownfield.ai is designed for early screening. It can help lenders understand whether a property has obvious environmental red flags before ordering formal environmental due diligence.

What if Brownfield.ai finds a red flag?

A red flag does not always mean the loan cannot move forward. It means the issue should be understood, documented, and reviewed to determine whether deeper due diligence, borrower follow-up, or consultant input is needed.

What if Brownfield.ai finds no records?

No records does not always mean no risk. Lenders should still consider site history, property use, surrounding properties, borrower information, and formal due diligence requirements.

Can the report be shared with borrowers?

Yes. The report can help organize borrower questions and clarify which records or site history details may need follow-up.

Can the report be shared with environmental consultants?

Yes. The report can help consultants and lenders focus on records worth reviewing. It does not replace the consultant’s formal evaluation.

Can Brownfield.ai help compare multiple properties?

Yes. Brownfield.ai is especially useful when comparing collateral risk across multiple properties. Teams can quickly see which sites appear cleaner, which need follow-up, and which may require deeper review.

Is Brownfield.ai only for brownfield loans?

No. Brownfield.ai can help screen many types of commercial real estate properties, not just known brownfields. It is useful whenever environmental risk could affect collateral, underwriting, financing, or redevelopment plans.

How fast do I get results?

Most searches return results in minutes. Enter an address, run the search, and get a clear report your team can review before spending money on deeper due diligence.

Do I need to talk to sales first?

No. You can create a free account, enter an address, and run your first property search without scheduling a call.

Who should use Brownfield.ai?

Commercial lenders, credit teams, loan officers, SBA lenders, community banks, commercial mortgage brokers, attorneys, consultants, and redevelopment finance teams can use Brownfield.ai to identify environmental risk signals earlier.

Can Brownfield.ai tell me if a property is safe collateral?

No tool can guarantee that from public records alone. Brownfield.ai helps identify known risk signals so your team can make a more informed decision and know what to investigate next.

Why not just wait for the Phase I?

You can — but by then, underwriting may already be underway, the borrower may be invested, and the timeline may be tighter. Brownfield.ai helps lenders spot obvious issues earlier.

Is the first report really free?

Yes. You can run your first property report for free, with no credit card required.

Screen the Property Before Environmental Risk Slows the Loan

Commercial real estate loans can be delayed by environmental questions — especially when risk is discovered late.

Enter any address and get a clear property risk report in minutes.

- First report on us

- No credit card required

© Brownfield AI

All rights reserved.